BALTIMORE

10075 Red Run Boulevard

Suite 401

Owings Mills, MD 21117

(443) 738-4900

FREDERICK

10 North Jefferson Street

Suite 200

Frederick, MD 21701

(240) 220-2415

BETHESDA

7315 Wisconsin Avenue

Suite 400W

Bethesda, MD 20814

(240) 220-2415

Trust Funding: Setting Your Trustee Up for Success

August 7, 2025

Diane Kotkin

A revocable living trust can serve as a valuable estate planning tool to help ensure that your finances remain well managed if you become incapacitated (unable to manage your affairs while you are alive) and to provide future financial security for your loved ones upon your passing. However, merely signing the trust agreement does not complete the estate planning process; to work properly, the trust must be funded.

What Is Trust Funding?

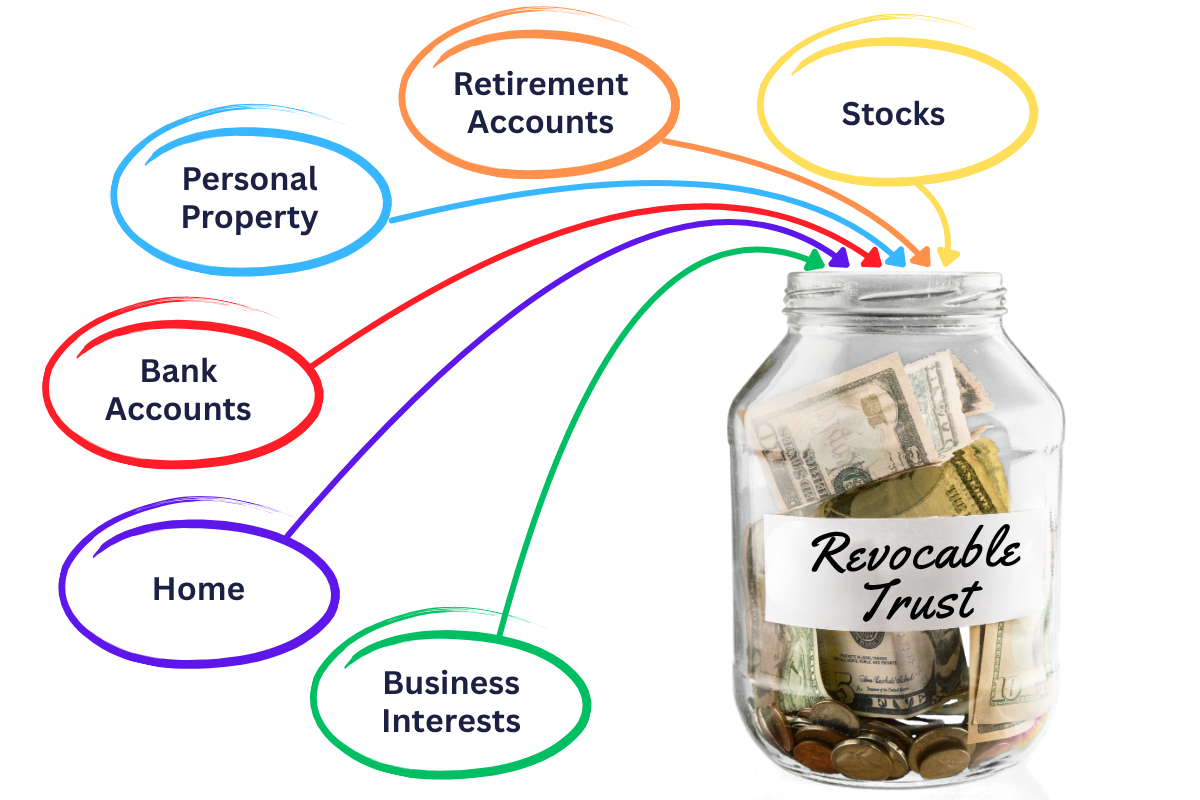

Trust funding is the process of transferring ownership of your accounts and property to the trust during your lifetime. For some accounts or pieces of property, it also includes designating the trust as a beneficiary so that the trust will receive ownership upon your passing rather than during your lifetime.

Trust Funding as a First Step for Trust Administration

A completely funded trust not only helps the trustmaker and their loved ones avoid the dreaded probate process but can also smooth the transition from you as trustee to your appointed successor trustee (the person you have selected to step in to manage your trust when you are incapacitated or have passed away).

- Accessing your accounts and property will be less complicated. If a trust is properly funded, your successor trustee should have little or no trouble stepping in to manage the accounts and property if you are unable to do so. This can be incredibly important if you are incapacitated and action regarding your finances must be taken right away. Your successor trustee may need to provide third parties with documentation evidencing their authority to act on the trust’s behalf. This documentation can easily be prepared by your attorney without court involvement.

- Creating the inventory for your trustee. One of the first things your successor trustee should provide to your named beneficiaries at your passing is a comprehensive inventory of all the trust’s accounts and property. If the ownership and beneficiary designation confirmations you gathered during the funding process are periodically reviewed and kept up to date, you will leave behind a helpful preliminary list for your trustee to use in creating the inventory, which can save the successor trustee time and frustration in the beginning stages of administration.

- Confidence that your plan will be carried out. One of the primary reasons to create a trust is to control what will happen to your accounts and property if you become incapacitated and after you have passed away. The instructions you leave in your trust apply to only those accounts and property owned by the trust (transferred to the trust either during your life or by beneficiary designation at your death). If an account or piece of property is not owned by the trust, the instructions in the trust agreement will not control what happens to it.

A Fully Funded Trust Helps Avoid Probate

If the item is not owned by your trust and is also not jointly owned or does not have a beneficiary designation other than the trust, it will likely have to go through the probate process. During probate, the account or property will, at best, be transferred through your pour-over will to your successor trustee as the trust’s new trustee. A pour-over will should be prepared with all trust-based estate plans. It states that all accounts and property in your probate estate are to be distributed to the trustee of your trust. Pour-over wills do not contain the specific details included in the trust (such as who will receive an inheritance from you and when and how they will receive it), so they do allow for some privacy. Although the instructions in your trust will eventually control what happens to any forgotten accounts or property, your loved ones will still have to go through the time-consuming and costly probate process. At worst, if you never created a will (pour-over or otherwise) or if your loved ones cannot find it, the court will rely on a state statute for dividing your money and property. The statute will generally provide for your surviving spouse, children, grandchildren, parents, and siblings, depending on who is living at your death. The downside of relying on state law rather than on a trust is that your accounts or property could be given to someone you intended to disinherit or whom you wanted to receive only a small share.

When Your Trust Will Not Control the Outcome

If a beneficiary other than your trust has been named on an account or piece of property, it does not matter what your trust agreement says. That account or piece of property will go to whomever is listed on the beneficiary designation. The same is true with jointly owned property. In most cases, when one co-owner of an account or piece of property dies, the surviving co-owner(s) automatically receive the deceased owner’s interest in the account or property upon their death. It is important that you know what your current beneficiary designations say and that they match your estate planning goals.

Working Together Now for Future Success

Creating a trust estate plan is just the first step. The last step you need to take is to fund your trust. Please call us if you have questions about this process. We are available to assist you in any way you need. If you would like, we are also available to handle the trust funding for you. Let’s partner to make sure that your hard work will set you and your loved ones up for a successful future.